Filevine

- Legal tech giants like Harvey and Filevine are buying startups to add new features to their software.

- The consolidation is driven by increased demand for legal software with more features.

- Smaller legal tech startups may face pressure to join larger companies or risk not getting traction.

Legal tech is entering its consolidation era.

Early signs are already visible. This week, Harvey, an $8 billion legal software giant, acquired Hexus, a sales tech startup built by former Google and Twitter (now X) engineers. Filevine, another major legal tech player, recently snapped up Pincites, a four-person startup that was an early Y Combinator bet on what has since become one of legal tech's hottest frontiers: artificial intelligence-powered contract drafting and revision.

And earlier this month, Microsoft quietly absorbed 18 employees from the legal software startup Robin AI after it filed for bankruptcy.

Industry executives say this is just the beginning. Early winners of the legal tech boom are expected to buy smaller companies to extend their leads and add new features to their software.

For teams in a crowded legal tech market, joining one of those platforms is increasingly attractive, said John Locke, a Filevine investor and partner at Accel, who leads the firm's growth fund. He believes Harvey and Filevine could both be significant public companies someday.

"They're now at a point where people look at them and say, 'I would like to join that fast train,'" Locke said.

Pincites wasn't looking for an exit.

The company was founded in 2023 by two sisters working from home. Sona Sulakian was a transactional patent attorney. Mariam Sulakian worked on GitHub Copilot, focusing on security. They saw a gap: Lawyers negotiate contracts inside Microsoft Word, but most AI tools lived elsewhere.

They built a Word plug-in lawyers actually used, and racked up customers including Redis, Glean, and Vercel. In 2023, Pincites raised a seed round led by Nat Friedman, GitHub's former CEO, and Daniel Gross, who, with Friedman, now works in Meta's superintelligence lab.

Investors encouraged the sisters to raise another round of funding. Then the inbound acquisition interest started.

At one point, there were at least five or six term sheets on the table, Ryan Anderson, Filevine's founder and CEO, said. The sisters initially waved them off.

What changed, both sides said, was familiarity. Filevine had already been a customer. Its internal legal team used the Pincites software for contract redlining — the process of marking up and revising contract drafts during negotiations — and pushed Anderson to take a closer look.

Founded in 2014, the Utah company now manages over 13 million active legal matters on the platform and sells software used by law firms, corporate legal teams, and government agencies. Its customers include Kroger, Goodwill, the Utah Jazz, and five state attorneys general.

Filevine has raised over $600 million in funding to date and was last valued at $3 billion.

What the company lacked was a next-generation redlining tool.

Some competitors, Anderson noted, promote redlining as a core feature. To compete for enterprise and mid-market deals, Filevine needed a comparable offering.

The entire Pincites team is joining Filevine and will anchor a new San Francisco office. Over time, the product will be folded into Filevine's system, creating what Anderson calls "a single pane of glass" where users can draft and edit documents, pull in context from other systems, and track time and billing.

For the Sulakian sisters, the decision came down to distribution. Pincites had more ideas than it had capacity to execute, they said, and expanding its customer base fast enough to capture the market would have required years of additional fundraising and hiring. Joining a larger platform offered a shortcut.

Pincites didn't sell because it was distressed, Mariam said. "We would have been fine no matter what." It sold because the market is maturing.

After years of experimenting with narrow, single-purpose tools, law firms and in-house legal teams are looking to simplify, Sona said. Managing a patchwork of apps became costly and unwieldy, particularly for smaller firms.

That pressure is now driving a "shakeout of point solutions," said Omar Haroun, cofounder and chief executive of the legal tech company Eudia.

"The winners will be platforms embedded in daily legal workflows and tied to outcomes," Haroun said. "The rest will be acquired, merged, or phased out."

That dynamic mirrors what played out during the rise of mobile software. Smartphones unleashed a wave of narrowly focused apps, made possible by cheap development and easy distribution. But as platforms matured, users tired of app sprawl, and the biggest companies began bundling features or buying competitors outright. Facebook acquired Instagram and WhatsApp. Google bought Waze.

Legal tech now appears to be entering a similar phase, as large language models lower the barrier to building these tools — and raise the bar for surviving as a standalone company.

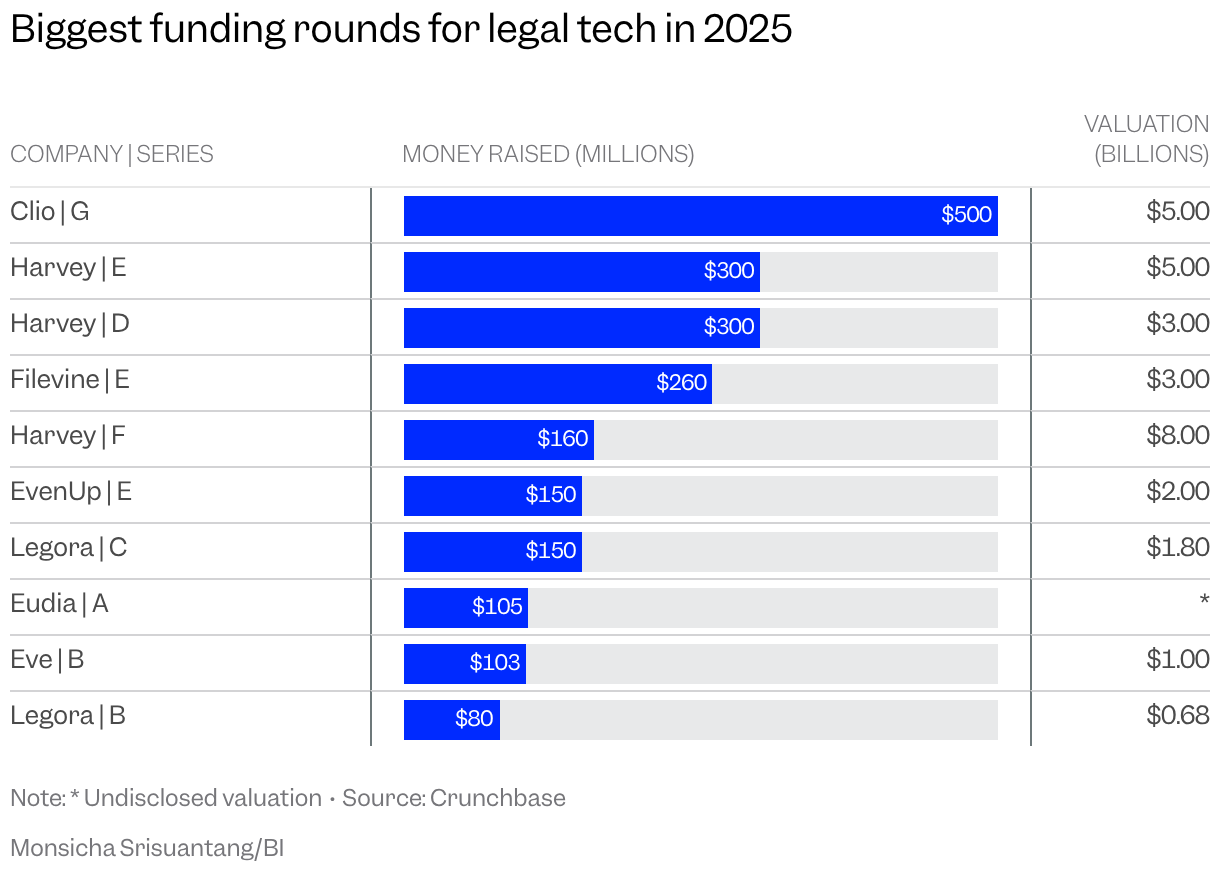

Over $4 billion flowed into startups building technology for lawyers last year, nearly double the amount raised the year before, according to Crunchbase. More than a third of last year's investment went to just three companies: Harvey, Filevine, and Clio, which sells software used by law firms to track cases and send invoices.

Last year, Clio scooped up the legal research platform vLex for $1 billion, part of its push to become the system of record for small and midsize firms.

With that concentration of capital comes pressure. The biggest players have to deploy it. And smaller startups have to prove they can hold their own. For some builders, the choice may increasingly be to sell — before the window narrows further.

Have a tip? Contact this reporter via email at mrussell@businessinsider.com or Signal at @MeliaRussell.01. Use a personal email address and a non-work device.